Do travel retailers fully appreciate the smoke-free dynamic? By: Peter Marshall

Travel retail has embraced the language of “smoke-free” and “next-generation”, but the numbers suggest the shift may be happening faster than the industry itself.

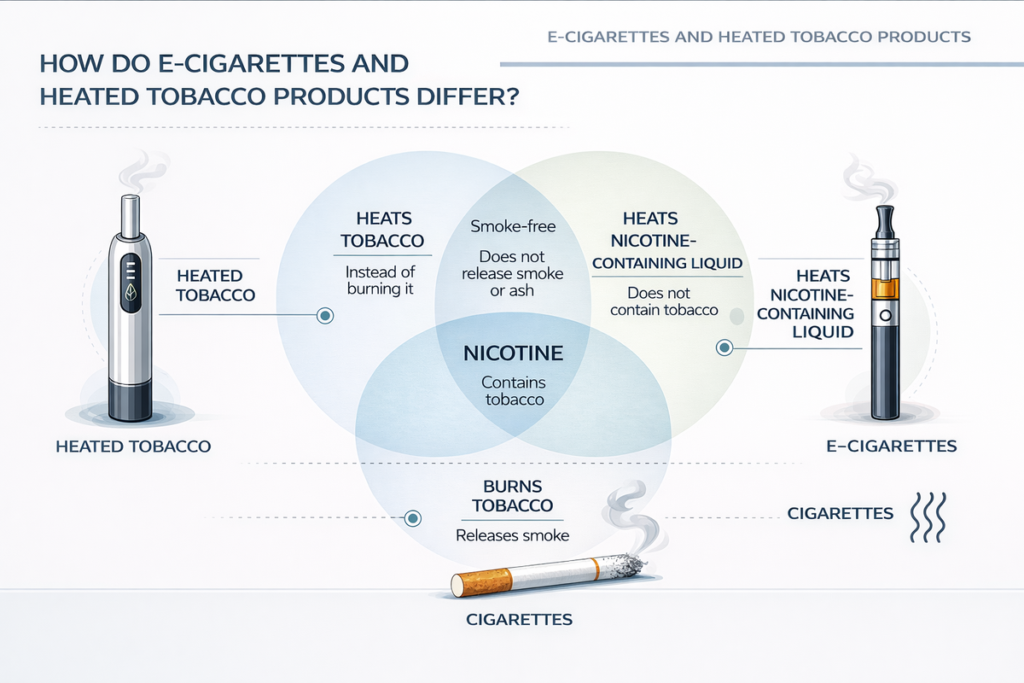

Across global markets, combustible tobacco is slowing while reduced-risk alternatives – from heated tobacco to nicotine pouches – are growing at pace. Suppliers are reorganising around smoke-free portfolios, yet in many airport stores the category still looks anchored in cartons rather than a broader nicotine ecosystem.

As smoke-free alternatives gain traction, travel retail has an opportunity to guide adult consumers through new formats and missions. The question is whether the sector is moving quickly enough to capture that growth – or simply watching it unfold elsewhere.

Travel retail knows the language of “smoke‑free” and “next‑gen” – but you could well argue it still hasn’t really internalised what the numbers are saying.

Global and category data now point in one clear direction. The global tobacco market is forecast to grow only modestly – around 2.5% CAGR to 2034 – as cigarettes plateau or decline in many markets. Within that, safer nicotine and non‑combustible formats are doing the heavy lifting. The latest Global State of Tobacco Harm Reduction (GHTSR) report notes that at least one category of safer nicotine product (vapes, heated tobacco, snus or nicotine pouches) is now legally available in 129 countries, and that substitution away from combustible products is gathering pace. Harm‑reduction analysts go as far as to say that, if fully realised, switching from smoking to less harmful nicotine products could deliver one of the biggest public‑health gains of this century.

Travel retail tobacco sits right in the middle of that shift. But at times it still behaves as if it were on the sidelines. According to a recent global travel‑retail tobacco study, the channel was worth about USD 8.0 billion in 2024, after a flat to slightly negative CAGR of roughly −1% since 2019. The same report forecasts an acceleration to USD 13.5 billion by 2029 and USD 21.5 billion by 2034, at around 10–11% CAGR through the next decade. The interesting part for airport retailers is where that growth is expected to come from. Cigarettes may still represent just under half of value today – about 49.7% or USD 4.0 billion in 2024 – but “next‑generation products” are projected to be the fastest‑growing segment, with a forecast CAGR of about 14.2% between 2024 and 2029.

The suppliers’ P&Ls tell the same story. Philip Morris International reports that smoke‑free products – its definition includes heated tobacco, oral nicotine and e‑vapor – accounted for 41.5% of its adjusted net revenues in 2025, up from 38.7% in 2024. That translated into smoke‑free shipment growth of about 12.8% and net revenue growth of 15%, versus just 1.4% volume growth across all products as cigarette volumes declined. Crucially for this channel, PMI singled out travel retail as one of its strongest‑performing smoke‑free channels in 2025, with airports delivering the highest year‑on‑year IQOS consumables growth of any market worldwide.

In Q4 2025, PMI Global Travel Retail reached a 19.5% heated‑tobacco share across airports where IQOS is listed, a gain of 3.5 percentage points in just twelve months.

At the same time, British American Tobacco’s (BAT) results for the year ended 31 December 2025 underline the same structural shift. The company added 4.7 million consumers to its smokeless portfolio, bringing the total to 34.1 million, while smokeless products accounted for 18.2% of Group revenue. Revenue from BAT’s New Categories – spanning vapour, heated products and modern oral nicotine – returned to double-digit growth in the second half of the year, supported by strong performance from the Velo oral nicotine brand across multiple regions. New Categories contribution rose sharply to £442 million, reflecting the company’s continued focus on quality growth and premium innovation.

In the USA, nicotine pouches delivered particularly strong momentum, with Velo Plus achieving triple-digit revenue growth and helping Velo reach the number-two position by both volume and value share. The brand also achieved category contribution profitability within one year of launch – a milestone that underlines both consumer uptake and improving economics for reduced-risk formats. BAT also highlighted three premium innovation launches – Vuse Ultra, glo Hilo and Velo Shift – as key drivers of future growth, reinforcing the company’s long-term pivot towards smoke-free and non-combustible nicotine categories.

Further data from Philip Morris International reinforces that this is a structural transition rather than a sudden disruption. In its 2025 Change in Motion Value Report, PMI notes that smoke-free alternatives – particularly heated tobacco – continue to expand rapidly, with international volumes growing at around 12% CAGR over the past three years. At the same time, cigarettes remain widely available, underlining a long-term coexistence between categories. For travel retail, the implication is clear: reduced-risk formats are expanding the overall nicotine category, creating incremental opportunities rather than simply replacing existing sales.

Step back and the pattern is clear: the global combustible market is slowing, smoke‑free is growing at double‑digit rates and travel retail is one of the hottest smoke‑free theatres. Yet in many terminals, the store layout still tells a 2010 story, not a 2030 one. The cigarette wall remains the hero and is largely regarded as a money-generating commodity. Next‑gen formats – heated sticks, devices, pouches – are often tucked into a compact “innovation” bay or device counter, competing for visibility with duty free’s traditional carton‑stacking mentality.

Part of the problem is that many travel retailers still view non‑combustibles as a tactical extension to the tobacco range rather than as the core growth engine of a broader nicotine category. Data from harm‑reduction analysts make that broader shift explicit. Reduced risk nicotine products are gaining increasing share of nicotine users, with heated tobacco taking substantial share in markets like Japan, South Korea and parts of Europe as cigarette volumes fall. In parallel, the oral nicotine and pouch segment has exploded, with global pouch volumes and revenues climbing sharply, particularly in Europe and North America. These are not marginal line‑extensions. They are where new, incremental value – and often adult users – are going.

The travel mission amplifies this. Long‑haul flights, smoke‑free hotels and business trips are exactly the occasions where discreet, odourless and device‑based nicotine products solve a real problem for adult users. But most airport tobacco zones are still optimised for the old “carton for home” mission: one big wall, price‑per‑carton communication, and staff primarily trained to up‑trade pack buyers into bigger formats. If “smoke‑free” is really a strategic pillar, the merchandising and training should reflect very different shopper missions: trial, device onboarding, top‑up for frequent users, and help navigating cross‑border rules.

Regulation is the other brake, and retailers raise it quickly – often with justification. Customs and duty‑free regimes were written around combustible tobacco and grams of leaf, not milligrams of nicotine in a pouch or stick. Allowances, warning standards and even basic classification are clearer for cigarettes and cigars than for HTPs, vapes or pouches on many routes. The latest GSTHR analysis notes a patchwork of regulatory responses worldwide, from supportive harm‑reduction frameworks in markets such as the UK and New Zealand to outright bans or severe restrictions elsewhere. That patchwork makes some operators understandably cautious about betting the category on products that may face sudden policy shifts.

Regulation is the other brake, and retailers raise it quickly – often with justification. Customs and duty‑free regimes were written around combustible tobacco and grams of leaf, not milligrams of nicotine in a pouch or stick. Allowances, warning standards and even basic classification are clearer for cigarettes and cigars than for HTPs, vapes or pouches on many routes. The latest GSTHR analysis notes a patchwork of regulatory responses worldwide, from supportive harm‑reduction frameworks in markets such as the UK and New Zealand to outright bans or severe restrictions elsewhere. That patchwork makes some operators understandably cautious about betting the category on products that may face sudden policy shifts.

Industry data also points to a regulatory imbalance shaping category development. According to PMI’s 2025 Value Report, more than 190 million adult smokers across over 20 markets still lack legal access to smoke-free alternatives, despite cigarettes remaining widely available. The same analysis indicates that combustible volumes decline faster where smoke-free products are accessible, while cigarette volumes have grown in some markets where alternatives are restricted. For travel retail – operating across multiple regulatory frameworks – this creates both complexity and opportunity, particularly as airports increasingly serve as discovery environments for evolving nicotine options.

But – importantly – the same data also shows that where regulators do differentiate less harmful nicotine products from smoking, smoking rates are falling faster. And smoke free alternative products are gaining share. For a channel that prides itself on being the showcase for global brands, “waiting for certainty” risks becoming a polite way of standing still while domestic markets move on. Travel retail has an opportunity to be the place where adult smokers encounter – and understand – smoke‑free options in a controlled environment with trained staff and clear information.

In fairness, some players are already moving. A number of leading airports now feature dedicated next‑generation bays and branded heated‑tobacco boutiques, supported by targeted digital communication and concierge‑style staff who can explain devices, usage and border implications. Market forecasts are explicit: if travel‑retail tobacco is going to more than double over the next decade, next‑generation products will be a disproportionate part of that story. Suppliers are reorganising around smoke‑free – PMI’s business is already over 40% smoke‑free by revenue, and in some European markets smoke‑free exceeds 50% of its total regional net revenues.

In fairness, some players are already moving. A number of leading airports now feature dedicated next‑generation bays and branded heated‑tobacco boutiques, supported by targeted digital communication and concierge‑style staff who can explain devices, usage and border implications. Market forecasts are explicit: if travel‑retail tobacco is going to more than double over the next decade, next‑generation products will be a disproportionate part of that story. Suppliers are reorganising around smoke‑free – PMI’s business is already over 40% smoke‑free by revenue, and in some European markets smoke‑free exceeds 50% of its total regional net revenues.

For suppliers and retailers alike, the shift is increasingly framed not as a binary choice between traditional and next-generation products, but as an opportunity to expand the total nicotine category. As BAT and PMI both emphasise, smoke-free growth is bringing new adult consumers into the category, creating incremental value and new shopper missions – particularly relevant in the travel retail environment.

So, the question is this: do travel retailers want to ride that curve or follow it at a distance? Recognising the trend is arguably no longer good enough – the numbers now require conviction. That means planning 2029 shelf space on the assumption that smoke‑free is the growth engine, not an interesting annex. It means designing category architecture around nicotine missions, not historic tobacco norms, and it means investing in staff training and digital content that position the duty‑free shop as a credible guide through a more complex nicotine landscape.

In other words: if your tobacco zone still looks like a cigarette shop with a smoke‑free corner, all the data is telling you it is time to flip that script.

To subscribe free, please enter your email address: