Avolta’s Financial Year Results: Is Contraction In North America Set To Last? By: Luke Barras-Hill.

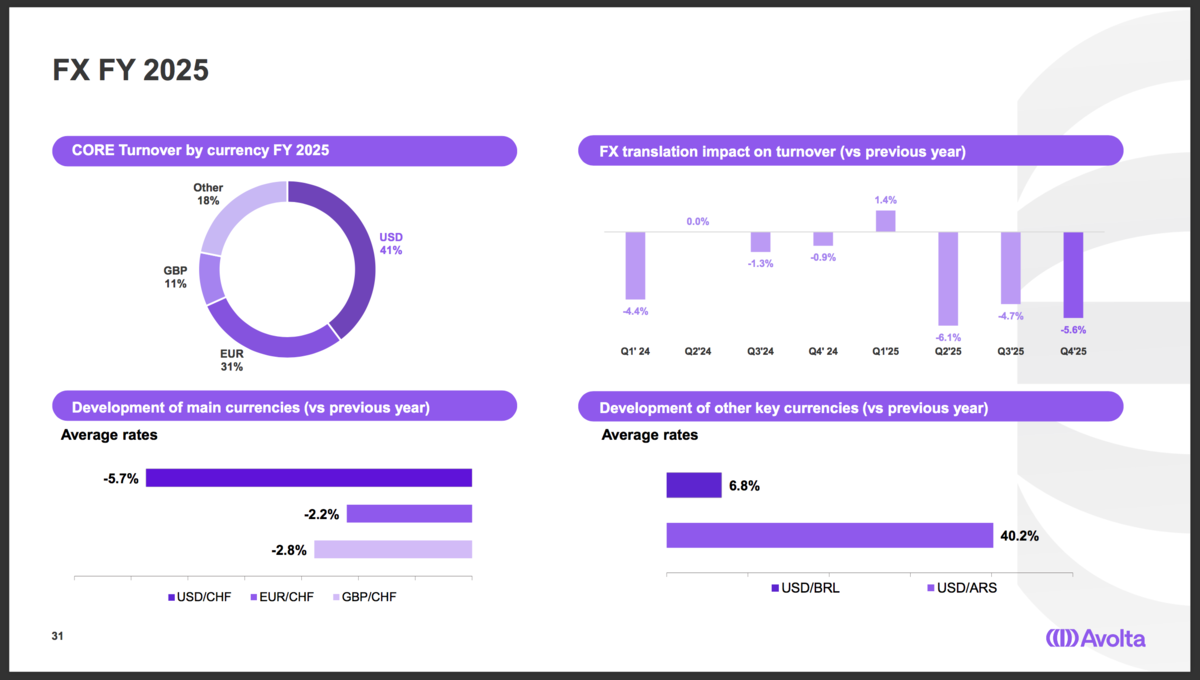

Last month, Avolta announced its full-year 2025 results. Core turnover grew 5.9% year-on-year to CHF 13,720 million* at CER (+5.5% organic). Core EBITDA reached CHF 1,324 million, with EBITDA margin at 9.7% (+0.3% yoy).

Asia Pacific led growth (+44.4%), while EMEA (+3.0%) and Latin America (+1.5%) gains were modest. However, Avolta’s decline in North America (-5.8%) stood out.

In his first feature for TRunblocked.com, Editorial Contributor Luke Barras-Hill examines the company’s regional performance, travel and spending mechanics and the push-and-pull factors influencing what are nascent recovery glimmers into 2026.

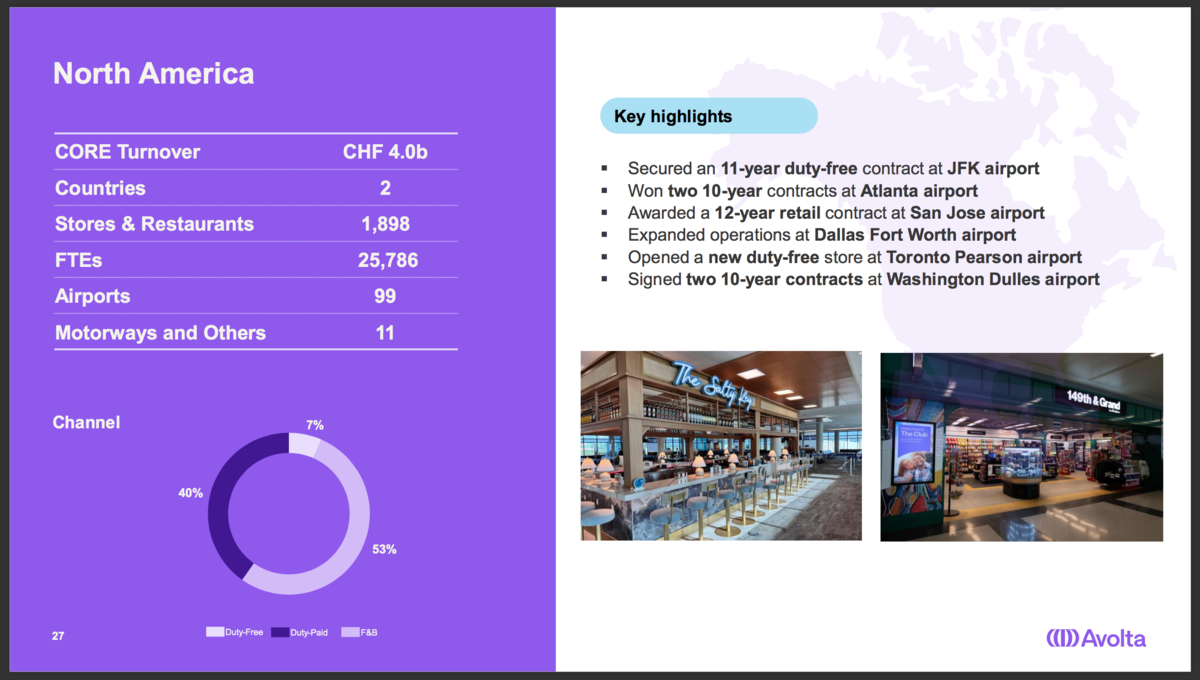

In a region accounting for nearly a third (30%) of the global business, North America turnover hit CHF 4,049m [2024: CHF 4,297m] against a ‘softer backdrop’ for operations.

Avolta oversees approximately 1,898 shops and restaurants across 99 North American airports in a market skewed towards duty paid (40% of turnover) and domestic traffic (around 90%). F&B generates 53% of income, with food, confectionery and catering the main contributors.

Dollar weakness, cautious travel recovery

Q4 turnover fell 7.1%, marking a third consecutive quarterly decline for what has long been a dependable performer. There are a myriad of reasons behind this. Currency volatility has not helped, say analysts.

The US dollar shed approximately 12% in value against the Swiss Franc last year – a steep decline by recent standards. In a results presentation, Avolta pointed to a 5.7% decline year-on-year in USD/CHF average rates, which compares to a lesser 2.2-2.8% negative impact against Euro/CHF and GBP/CHF equivalents [Ed – note the likely difference between average and spot rates used to calculate the USD/CHF FX effect].

With 41% of turnover in US dollars, exposure to currency movements can amplify the translation impact.

“Although North America accounts for roughly 30% of Avolta’s revenues, almost half of sales are USD-denominated,” Manuel Lang, Equity Analyst, Bank Vontobel told TRunblocked.com. “That FX drag alone explains most of the reported decline, and we expect an even bigger 6-7% headwind this year if the dollar remains weak.”

Signs of cooling growth in North America can be traced to Avolta’s full-year 2024 results. And in 2025, the travel data did not flatter. The Basel-headquartered travel retailer acknowledged the ‘slowdown in US passengers’ among a mix of external headwinds weighing on what was otherwise a ‘resilient performance’ that year.

According to Oxford Economics, international overnight visits to the US declined 5.7% last year, coloured by shifting travel sentiment, exchange rate shifts and President Trump’s tariff-related economic pressures amid intensifying global trade tensions.

In a recent briefing report validating downside scenarios modelled last year, Oxford Economics estimated a 25.7% fall in visits from historically significant travel and trading neighbour Canada.

Despite an approximate 8.6% uptick in arrivals from Mexico, overseas visits (excluding Canada and Mexico) fell 2.5% in 2025. Tellingly, more than half of that deterioration was linked to Western Europe.

In the company’s nine-month 2025 results, reported growth in North America fell 5.4%, though at the time Avolta reported ‘encouraging inflection’ for the region.

Indeed, passenger volume and spend per pax helped lift the region’s form in Q4, with ‘nice traction’ witnessed in Q1 2026 linked to key sales periods including the US Spring Break, Easter and Ramadan.

In comments shared with TRunblocked.com, Yves Gerster, CFO, Avolta commented: “The softer growth in North America relative to other regions through much of 2025 was primarily driven by lower passenger volumes, though we have seen encouraging improvement more recently in Q4 and into early 2026.”

This corroborates signs of cautious improvements in the US, as referenced by Avolta CEO Xavier Rossinyol during an earnings call in March.

So what about the international travel picture into 2026? According to leading aviation data provider OAG, total estimated international seat capacity to North America (USA & Canada) is broadly flat (-0.2%) in Q1. However, US-Canada seat capacity is down approximately -10% yoy for the quarter, reflecting the ongoing brittleness between both countries.

“The Latin America market has seen some growth as airlines fortunes have improved in that region over the last year,” observed John Grant, Chief Analyst at OAG.

On the near- to mid-term outlook, Jon Cox, Head of Swiss and European Equities at Kepler Cheuvreux echoes “signs of improvement” for the region, while Oxford Economics forecasts a 3.9% increase in international inbound travel to the US in 2026.

“With average ticket spend in the region trending upwards, we expect a modest recovery in US travel through 2026, supported by resilient consumer demand for experiences over goods,” added Lang. “The weak dollar now plays in the region’s favour, making the US more attractive for inbound travellers.”

Avolta stores should benefit this summer as major US hubs, plus Toronto and Vancouver Airports in Canada, capitalise on strong travel and spending demand ahead of the FIFA World Cup (11th June – 19th July).

“The medium-term outlook for passenger growth remains intact, supported by strong underlying industry fundamentals,” noted Gerster.

Geopolitical risks persist. However, Avolta’s Middle East exposure is limited (around 3% of global turnover), with geographical diversification in around 70 countries helping to mitigate regional shocks.

Shifting US concessions landscape

But the breadth of portfolio brings its own challenges. North America is not immune to rising airport concession fees, mix effects (nationalities, flight profiles etc.), evolving consumption behaviours and pricing sensitivity, despite typically durable local traffic. Market-specific leasing conditions (including ACDBE participation in US concession agreements) can make for an unpredictable trading environment.

Promisingly though, Avolta boasts a weighty concessions pipeline having won a slew of tenders in recent years. It has secured major new concessions at New York’s John F. Kennedy International Airport – an 11-year duty free lease at Terminal 8 being the most recent – Atlanta, San José and Toronto Pearson, among others.

Naturally these new contracts will take time to fully yield. The Bluechip contract at JFK Terminal 6 netted at the end of 2024 should provide some impetus in the quarterly numbers, with the first phase opening looming.

Elsewhere, structural forces are at play. DFS Group’s retreat from its historic US strongholds at San Francisco and Los Angeles International Airports and in Hawaii has shaken up the duty free tenancy landscape at US airports. Against this backdrop, Avolta will be looking to strengthen its commercial performance as travel trends improve.

Assortment ‘balancing act’

Retail hybridisation offers an important lens to capture trend-led consumer spending. To this end, the company has made a point of investing in blended retail and F&B concepts, technology and experiential formats to drive dwell time, engagement and spend.

This will help to leverage its gross profit margin while dampening the potential threat of dwindling per passenger spending in core retail of the kind witnessed in the European airports segment in recent years.

Looking ahead, Avolta has reiterated its mid-term outlook of 5-7% organic growth per annum and EBITDA margin improvement of 20-40 basis points.

“As travel conditions continue to improve, our focus is on translating this momentum into higher penetration, conversion, and average ticket through a combination of targeted commercial and operational initiatives,” explained Gerster.

“A key priority is further optimising our assortment, with a strong emphasis on local and premium products, while maintaining the right balance between convenience-led and experience-driven propositions.”

*Excludes net sales from the motorway fuel business.

To subscribe free, please enter your email address: