Britain doesn’t want to pay for Brexit. Is Travel Retail any different?

Does Travel Retail know what GDS means and what does a GDS think Travel Retail is?

The answer is simple, yet very complicated. Travel Retail to us, or at least those reading this blog, means the retailing of “Duty Free” related products in airports, on airlines or other travel mediums, like Cruises.

To a GDS, it means the selling (mainly) of bits of paper, or the digital PDF version, such as an airline ticket and all the associated Ancillary Revenues. These Airline revenues are now as long as your arm; seats, baggage, priority boarding, lounge access. You can even find and option for Oxygen and Firearms. Firearms, what’s that all about?

Oh, I forgot to explain GDS! (Global Distribution System).

Well, every time we book a flight, someone has to process this transaction by offering you the Airline, routing, prices, options and conditions. You might book through a Travel Agent, online or physical, or direct with the Airline. But, one way or another there is a GDS or a Booking Engine involved somewhere along the line. It is quite rare now for us to go to the airport ticket desk to buy a ticket like we used to do. It is now getting even rarer for us to pop down the High Street to a Travel Agent.

GDS are mostly “Commission Agents”, earning a buck or two on each transaction. Which, when grossed up for all those flyers, is a lot of money. Without going into some of the perennial wars that have evolved between GDS’s and their Airline partners, they figure in your travel life from the start of your journey and beyond. In fact, they can also figure in everything you need, such as Hotels, Car Hire, Catering, Lounges and Airport Fast-Track. A GDS thinks that “Travel Retail” means the Merchandising of all those bits of virtual paper. What it doesn’t think, is that “Travel Retail” means that selling of all those physical Luxury Goods to the Travellers of the Globe.

Amazingly, what GDSs don’t figure in or “Merchandise”, is your wish for that duty-free Chanel No 1, those Marlboros or that JW Black on the rocks, sipped at sunset from that exotic resort hotel you also bought from them!

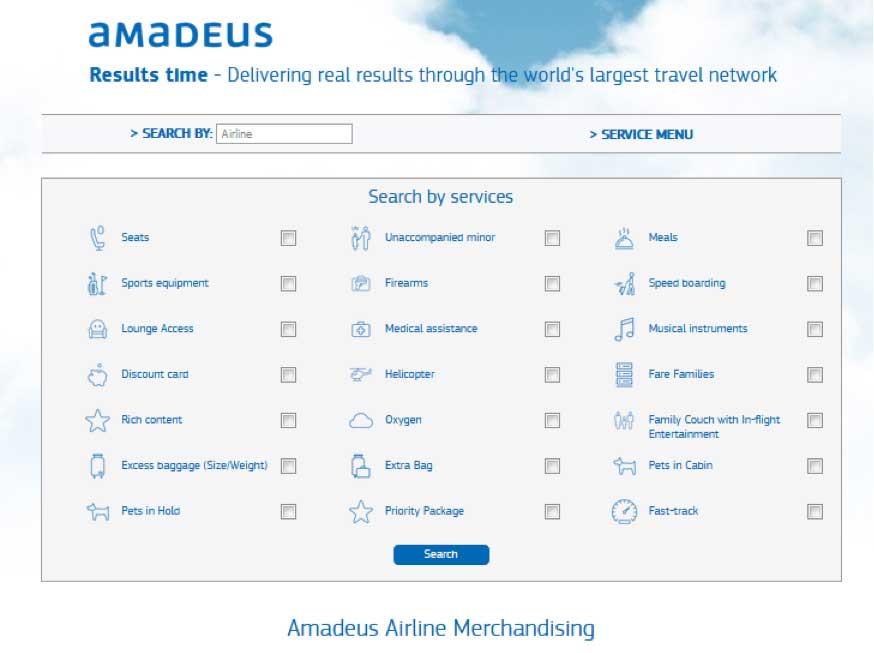

Amadeus and their Subsidiary, Navitaire are the largest of the GDSs, servicing multiple Airlines, be they Traditional Legacy or the modern day LCCs. Here is what Amadeus publish as their Global Ancillary product offer for their Partners….

Anyone spotted how “Duty Free”, “Tax Free” or any other form of traditional shopping is missing from the above list of options?

“Duty Free Shopping” is the world’s original Ancillary Revenue, it was way in advance of all those too clever by half unbundled items, like seats, cushions, bags, food or drinks. And, with a global revenue value approaching $80billion, it is probably the largest revenue source that the GDSs forgot to sell.

But why?

This is simple, Travel Retail, (that’s our TR) doesn’t know how to connect to GDSs and GDSs don’t understand how the fragmented Travel Retail market works. There is another major detail that still precludes any possible coming-together for mutual gain: Duty Free Retailers don’t get the concept of paying sales commissions to 3rd Parties who can generate incremental sales for them, unlike Hotels, Car Hire or even other Airport Services like Lounges.

These GDSs don’t work for nothing, why should they, but they will soon want a slice of all that Shopping revenue generated by the very people that bought tickets from them.

Meantime, the inflight Wi-Fi and entertainment market is gathering pace, Inmarsat are one of the leaders in this field and recently published a joint study (with the London School of Economics) predicting future revenue potential of up to $30billion once Airlines adopt an on board communications platform. This LSE report claims that shopping in and from the air will likely be one of the major revenue streams.

It might be, but at a cost. They too need to make a buck or two on each transaction to justify the implementation of their complex communication systems on aircraft.

Overlooking for a moment the broad assumption that we are all going to start shopping all night, whilst sat on a flight, (which this Author doesn’t think is credible).

But even if I am wrong, which Stores are these Wi-Fi systems going to link to, how and where?

In 2018, in-flight connectivity will be worth less than $1 billion to airlines, but that figure will rise to $30 billion by 2035*.

Airlines criss-cross the world to different destinations, catering for multiple Cultures and Languages, not to mention the various Customs and Regulatory complexities involved to facilitate such a cloud based retail monolith. Theory great, practice a likely nightmare.

Instigating such a concept or platform for Travel Retail is not quite the same as it is for your mega retailers, like Amazon or eBay do already, because the entire expectation of most Consumers sat on a plane is that their goods should be duty-free or tax-free and this is before we consider the complexity of delivering goods across borders is addressed.

The LSE sneaked in “Home Delivery” into their report and (for sure) Amadeus and the other GDS Players will also start to grasp the mettle soon.

They already are, think laterally here as to what is a “Trip”.

And yes, Airbnb already have, see this job offer, Experience Expert.

“We are looking for a Trips and Experience Hunter … in charge across Global Markets”.

So what’s a Global Experience?

Isn’t “Duty Free Shopping “ a Global Experience and wasn’t it the first?

So, let us Travel Retailers (that is), sit here looking out for once and not looking within.

In essence, the Players that have the digital Travel Traffic are the ones that progressively rule the roost. GDSs, Online Travel Agents, Booking Engines and all those Blogs, Travel Publishers and Websites that feed off them and their Inventories for profit, are in control. Not to mention Google, Yahoo, Facebook and Twitter, or those Data Miners like Datalex, Open Jaw or Boxever.

As it stands, Travel Retail is out there on a limb, (frankly) trying to get something for nothing in the big wide digital world and (mostly) without the sophisticated reservation and selling tech that Marriott, Hertz, Lounge Key or Axa might have.

So where is all this going and who will gain in the end?

It is going to Downtown Stores and probably not to the duty-free or tax-free ones!

Why, because Debenhams, El Corte Ingles, Walmart, Bloomingdales, Tangs, KaDeWe or Galeries Lafayette are already there in digital selling terms. Many do Affiliation, which is a euphemism for “yes, we pay commissions if you bring us Customers”. They have pick-up points well organised and stores all over the place. They understand Partnership Relationships and employ staff who do this very thing. How many Travel Retailers currently have a Partnership or Affiliate Executive?

On reflection, I think the LSE might be right, they have to be, because someone is going to have to pay for all those satellites. And those GDSs need to find more money, so to replace all those bucks that the likes of Lufthansa are trying to claw back from them.

This means that all those super sophisticated Travel Tech Operators will need to “go find the money” and quick.

But, they ‘aint going to do that with those that don’t want to pay, haven’t got an api and not yet structured their offer to explain what they can sell, where how and under what rules and regulations.

The Digital threat for Travel Retail, so clearly outlined some time ago by Julian Diaz of Dufry is now on the doorstep and it isn’t going to be seen off by churning a few messages on Facebook or Twitter every day.

Sabre, Trip Advisor or Kayak are certainly going to bring those Travellers their Shopping sometime soon… and deliver it to them too.

Almost certainly from a store near you, but with even more certainty, not from and airport, airline, cruise or ferry boat store near you. Time will tell, let’s hope I am wrong!

*Courtesy “Sky High Economics” 2017 Report London School of Economics/Inmarsat

About: Ivor Smith launched www.dutyfreeonarrival.com almost 10 years ago as the first search database for Duty Free stores. He is now adapting this to facilitate a system whereby Travel Retail can fit together with Travel Retail for beneficial gain. How is this done? Oddly, it is not about Tech, but market knowledge.

To subscribe free, please enter your email address: